(Swans - September 20, 2010) Another mid-term election is looming in the United States. Next November, the electorate will choose the political team that in the midst of a recession and widely-held fears about the future will carry the day. One side will win. It matters not though, because neither of the two contesting political parties is willing to face reality: The U.S. is not in a so-called great recession. It is in a latent depression. What has stopped it from becoming a full-fledged depression has been the willingness of the elites, both under the Bush II and Obama administrations, to resort to age-old Keynesian policies to stem the hemorrhage -- soup kitchen lines have so far been substituted by government checks in the mail. Some argue that governments' actions have not been enough to stem the recessionary times. Others claim that too much has been done, and time has come to cut spending and taxes in order to let the economy run to its natural ever-growing self. Again, it matters not, whatever position is taken. Do or don't, the economy is not coming back, and it should not. The Republican plan to cut spending (an age-old endeavor) will only bring more pain and social devastation. The Democratic plan to pump up the economy through deficit spending will only delay the actuality that the bind we all are in is a Catch-22. The economy that we have been used to in the past half-century is simply not going to come back. This three-part analysis will attempt to show the historical making of the dire and deepening crisis we all face, then try to demonstrate why the past paradigm won't and shouldn't come back, and end with a few suggestions that hopefully will lead to a future that is not predicated on the dead end the few want the many to embrace.

To fully grasp the extent of the current crisis one needs to take a short and much abridged walk through history. Human relationships have long been a story of antagonisms among the haves and the have-nots. In the feudalism era sharecroppers and peasants were peons of landowners and the divine royalties. The rise of the entrepreneurial class with the advent of the Industrial Revolution and capitalism led to a (often violent) change in leadership. The bourgeoisie overthrew the old order and the working masses migrated from the land to the mines and the factories and the shipyards, etc. Working conditions were execrable and the exploitation of the laborers was so prevalent (1) that they benefited the happy few and led to la belle époque, the Gilded Age, for the moneyed class whose rate of profits was very high and to labor demands for more equitable sharing of the created wealth and humane working conditions -- demands that were met with recurring violent and bloody repressions. The class struggles, which can be defined in layman's terms as profits for the few vs. the well being of the many (and private property vs. collective ownership), became the order of the era, increasingly influenced by political economists and philosophers. (2) The 1917 Russian Revolution threatened the moneyed class more than ever even though their hold on power with its resulting excesses in the accumulation of wealth could not be tamed until the Great Depression hit. In its wake, reformists like FDR and socialist parties in Europe cut their feathers substantially. Progressive taxation on income, estate, and capital was put in place; salaries among the wealthiest and the average workers trimmed from a ratio of about 400:1 to 30:1; social programs instituted... It must be remembered that workers' rights, unions, public education, health care, Social Security, public services, women's rights, civil rights, secular regimes, etc., are all a legacy of the left, which shed so much blood and tears to achieve these gains (even though the record ought to be tempered by the same left's avocation of the "civilizing mission" in far away lands -- i.e., colonialism). Nonetheless, the moneyed class became so worried about the loss of their privileges and the spread of socialist ideas that they, in Europe and in the U.S., supported Mussolini's Fascism and Hitler's National Socialism until well into World War Two when Hitler, instead of focusing on their interests -- the destruction of the Soviet Union and communist expansion in Europe -- launched an attack on their own countries and interests.

In 1945, Europe lay in ruins, its infrastructure and industries devastated, its people impoverished, lacking food and services (like electricity and water). Communist parties, particularly in France and Italy, gained strong traction and the influence of the Soviet Union loomed large. Threatened by the advance of leftist ideas, the powers-that-be chose to join them half way. Western elites devised a reconstruction plan based on Keynesian-Fordism -- state control and planning of the economy to varying degrees, mass post-Taylorism production, progressive taxation, collective bargaining through strong unions, and the transfer of gains in productivity to the salaried work force in the form of higher wages, which greased the wheel of demand for industrial production. The USA was an intimate participant in that process through the European Recovery Program (the Marshall Plan) passed by Congress in 1947, which was motivated by three objectives: First, to create new markets for American products (the U.S. was producing 55% of worldwide manufactured products in 1945 and feared a potential domestic recession could happen if new markets were not developed). Second, to neutralize and work against the growing influence of the Soviet Union and the Communist parties in Western Europe. Third, an altruistic desire to alleviate the dire conditions Europeans faced...which could lead to social unrest and bring on political developments that its second objective aimed to prevent (American idealism has always been mated with a heavy dose of pragmatic self-interest).

That political-economic plan was apt enough to generate what has been known, with some exaggeration as facts show, (3) by Jean Fourastié's famous saying: les trente glorieuses (the "thirty glorious years"). By the late 1960s, Keynesian-Fordism was running out of steam and in the wake of the 1973 oil crisis stagflation became the order of the day. In the atmosphere of malaise that took over the Western world, long-time opponents of Keynesian-Fordism found ready followers. Free-market evangelists like the classical liberals Friedrich Hayek, the author of The Road to Serfdom (Routledge, 1944), Milton Friedman of the Chicago School of Economics, the Randian Ludwig von Mises, and others (Karl Popper comes to mind) (4) became the intellectual force behind post-Fordist globalization (5) as they advocated their ideology -- low taxes, small government with minimal interference in the economy, little regulations if any, no redistributive policies that could lead to any kind of entitlements, individualism, free will, etc. By the early 1970s Keynesian-Fordism had by and large been nailed into the dustbin of history. In 1979, Margaret Thatcher became the British prime minister, and in 1981, Ronald Reagan the president of the United States.

Frédéric Lordon, a French economist and research director at the National Center of Scientific Research (CNRS) has called this historical reactionary watershed the reconquista of the moneyed class. (6) It must be noted that during that period -- approximately 1965-1975 -- the national corporations that were answering to and constrained by their respective governments turned into transnational entities (what was then called multinationals). Their allegiance was increasingly answering to the interests of their shareholders and no longer to the political whim or the demands of their workers. Coupled with the internationalization of the financial services, the moneyed class, les possédants ("those who possess") as Lordon calls them, were now in a position to blackmail the political class -- besides, concurrently, bribing it through campaign contributions. "If you do not lower our taxes we can move our headquarters to another country," threatened the managerial class, adding, "if you do not allow working flexibility and deregulate industry, we'll relocalize in more favorable climates." Finally, they concluded in a crescendo, "you politicians have to get rid or substantially lower social services, those dreaded entitlements."

Bought politicians and heedless governments relented. The age of detaxation and deregulation had begun in earnest. Taxes were smashed; (7) regulations were lessened; working flexibility -- a neutral expression to mean the contraction of wages and hiring/firing at will -- was instituted, and trade unions weakened. As Lordon reminds us, the goal was to starve the beast but the beast (the workers) was not willing to starve and kept fighting heartedly for the rights gained over a century of blood and tears. The result: public debt. What taxes did not finance any longer was substituted by national debt. Wealth was being transferred from the whole to the few though a simple mechanism -- financial gains for the few, debt for the many.

How could the masses get on board with this scheme? It had little to do with the so-called unsophisticated and uneducated masses (the Mises/Rand paradigm) -- though disinformation has been a part of the tragedy. Of late, a few mainstream economists and commentators (e.g., Robert Reich, Paul Krugman, Michael Hudson, Bob Herbert, et al.) have documented that wages have been remaining flat for about forty years (8) while, writes Reich, "In the late 1970s, the richest 1 percent of American families took in about 9 percent of the nation's total income; by 2007, the top 1 percent took in 23.5 percent of total income." (9) The facts are slowly seeping out. Yet, they appear to have not reached the consciousness of the overwhelming majority of the people. Why? Of course, there have been relentless PR campaigns vaunting trickle-down economics, the rising tide lifting all boats, the influence of the Laffer curve on the partisans of supply-side economists, and all other shibboleth lines, for example "freedom" and "greed is good." But objective socioeconomic conditions have been in play, which served to hide reality from reaching consciousness.

What happened can be seen in how the American elites handled the reconquista. Let's take a look at it in the United States. First, as Reich states, "women streamed into the paid work force. By the late 1990s, more than 60 percent of mothers with young children worked outside the home (in 1966, only 24 percent did)." Second, people started to work longer hours. However, these two factors were not enough to keep households ahead, and the elites were fully aware that a discontented populace tends to translate into social unrest. So, a devilishly smart scheme was devised, based on credit and real estate.

After a long decline that began in the mid 1960s the rate of profits bottomed out in the early 1980s before ascending again (see note #3), a result of stagnating wages and therefore wealth transfer to the rich. Yet, the economy was in recession with high inflation and unemployment (the latter reaching 10.8% in December 1982). The inflation was eventually tamed through the drastic policies enacted by the Fed under the chairmanship of Paul Volcker, which benefited creditors; further tax cuts were passed (1984 and '87), which benefited the wealthy; and access to credit was vastly expanded, which permitted the vast majority of households to keep afloat -- for a while. Credit cards multiplied like enzymes (10) as did consumer credits. Everything could be purchased on credit (vehicles, home appliances, students' fees, etc.). Private debts skyrocketed. Still, it was not enough to keep the economy growing. Policies to help the value of real estate rising indefinitely and home ownership enlarged were deliberately put in place by both Republican and Democrat administrations. These policies can be traced back to the New Deal, but were widely expanded from the 1970s onward. Home ownership as part of economic security and the realization of the American Dream became the major engine of the economy. It was achieved through a mix of fiscal and monetary policies (11) and access to easy credit guaranteed and securitized by Government Sponsored Enterprises -- the best known being Fannie Mae and Freddie Mac -- and governmental agencies such as the Federal Housing Administration, which is a part of the Department of Housing and Urban Development and others (e.g. Ginnie Mae). These policies became increasingly financially "sophisticated" under the stewardship of Bill Clinton and George W. Bush. (12) The end result has been exceptional, that is, out of the ordinary: The value of real estate in the USA has risen spectacularly for four decades (except for a short and slight downturn in the early 1990s) with returns on investment superior to those of financial services (13) -- until the proverbial feces hit the fan in a combination of a series of perfect storms.

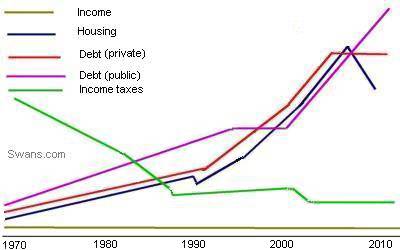

Let's recapitulate this short history with a graphical helping hand.

This graphic, developed in-house and certainly imperfect (for instance, it does not take into account the war economy that has been so dominant since WWII), brings together the various socioeconomic developments that have taken place in the U.S. and have led to the perfect multiple storms and the resulting wreckage to the world that will remain with us for years -- if not decades. The olive line at the bottom illustrates how wages, after steadily rising in the wake of WWII, have remained flat. The green line shows how taxes have abruptly been reduced for the benefit of the wealthy, which, in turn, have raised public debt (the pink line) as conflicting interests could not allow the slashing of social services and thus forced the moneyed class and its political companions (often the same crowd) to delay -- not forsake -- "starving of the beast," which they have relentlessly tried to accomplish for decades. (15) For the majority -- at least 80% of the American people -- the loss in wages was compensated by cheap credit and plastic debt (the red line), and since it was not enough to keep up with the Joneses and the PR, the very last recourse was to gamble on the rise of value in real estate (the blue line). Equity loans were taken out in abandon; mortgages refinanced not just once, but twice or more, in the belief that the value of property would keep rising forever. Much of the raised funds were spent on consumer products, vacations in exotic places, instant gratification, etc. A few borrowers attended to their children's needs -- the college tuitions that are bringing graduates to become debt peons even before they have entered productive life. Reich noted that "from 2002 to 2007, American households extracted $2.3 trillion from their homes." Money was of no concern. It grew on trees. One president advocated going to Disneyland and driving to the mall and to shop. A vice president asserted that deficits didn't matter. Any dissenter or skeptical observer was tagged un-American, thus ignored. Life was good, asserted the masters of the universe. People heard and wanted to believe the message and acted accordingly.

Sometime in 2005 cracks began to appear on Main Street. Households had maxed out their credit lines. The great wealth creation, it turned out, had been borrowed. The financial sector began to notice an increase in consumer defaults in 2006, which started to put a squeeze on their balance sheets. The burgeoning crisis moved to Wall Street. The meltdown took off in earnest with the Bear Sterns collapse in March 2008 and the FDIC seizure of IndyMac in July 2008. By the fourth quarter of that same year, Lehman Brothers was no more, AIG had to be rescued, Fannie Mae and Freddie Mac taken over by the government, and the financial sector had to be bailed out through the Troubled Asset Relief Program and huge interventions by the Fed. By then the crisis had spread to the entire world. Economic activity came to a screeching halt and business embarked on an abrupt deleveraging of its work force, thus compounding the damage done to the economy. The latent depression was in full force. It carries on to this very day.

The consequence can be seen, for anyone who is not blindly following a dismal ideology, that for decades le beau monde has peddled over the voices of reason -- and still does to this very day -- arguing that laissez-faire would bring heaven to earth. The result is here for all to see. Many will ask for more of the same in the name of sheer ignorance and emotional convictions based on an ideology they do not master, to the benefit of a class to which they do not belong -- not even considering the ecological bind that will bring us all to the realization that a paradigm change is not only required but needed if the survival of all species is a desired and chosen outcome.

[Author's note: In Part II to be published on October 18, 2010, we shall explore the reasons why the odds of the economy coming back to pre-crisis are nil, and why it should not come back.]

If you find Gilles d'Aymery's article and the work of the Swans collective

valuable, please consider helping us

Legalese

Feel free to insert a link to this work on your Web site or to disseminate its URL on your favorite lists, quoting the first paragraph or providing a summary. However, DO NOT steal, scavenge, or repost this work on the Web or any electronic media. Inlining, mirroring, and framing are expressly prohibited. Pulp re-publishing is welcome -- please contact the publisher. This material is copyrighted, © Gilles d'Aymery 2010. All rights reserved.

Have your say

Do you wish to share your opinion? We invite your comments. E-mail the Editor. Please include your full name, address and phone number (the city, state/country where you reside is paramount information). When/if we publish your opinion we will only include your name, city, state, and country.

About the Author

Gilles d'Aymery on Swans -- with bio. He is Swans' publisher and co-editor. (back)

Notes

1. For an example among many, see the 1850 internal regulations of a company located in Chaumont, France. (back)

2. To cite but a few: Saint-Simon, Fourier, Proudhon, Owen, Engels, Marx, Lenin, Luxemburg, etc. (back)

3. The model began to fall apart in the early 1960s when the rate of profit flattened before taking a plunge until the early 1980s -- a fact that is largely ignored by mainstream economists. For more on this topic, see "The causes of the post-war economic boom," International Review, October 29, 2008. The rate of profit and the dynamic of capital accumulation in capitalism are best understood and explained by people who are rooted in the Marxist tradition and knowledgeable enough to make sense of them -- a tradition and knowledge this author regrettably does not possess. (back)

4. George Soros's hero, Karl Popper, was one of the founders in 1947 of the Mont Pelerin Society, a society that advocates classical liberalism. Other founders included Milton Friedman, Friedrich Hayek, Ludwig von Mises, and George Stigler. (back)

5. For a more extended review of this topic, please see "Flexible Relations and Post-Fordist Globalization," by Taimur Rahman, chowk.com, April 23, 2003. (back)

6. "La dette publique, ou la reconquista des possédants," by Frédéric Lordon, Blog of Le Monde Diplomatique, May 26, 2010. For readers who can read French, this is the clearest exposé of events that have taken place in the past 40 years, which have decimated the masses for the benefits of the few. Lordon is to my knowledge the only economist that has been able to undertake a serious contextual analysis with an impressive sense of humor. Highly recommended. (back)

7. The trend toward lower taxes began earlier in the U.S. under the Kennedy administration. In 1963, Kennedy proposed a plan to lower income taxes across the board. The plan was passed in 1964 by the Johnson administration. All marginal tax rates were cut, the top one from 91% to 77%., then 70% in 1965, 50% in 1982, 38.5% in 1987, 28% in 1988, up to 31% in 1991, 39.6% in 1993, and 35% in 2003. See U.S. Federal Individual Income Tax Rates History, 1913-2010 at the Web site of the Tax Foundation. (back)

8. They actually have contracted. The latest Census data shows that "the median household income fell 0.7% to $49,777 in 2009, down 4.2% since 2007, when the recession started." (back)

9. "How to End the Great Recession," by Robert Reich, The New York Times, September 2, 2010. (back)

10. "Between 1989 and 2006, the nation's total credit card charges increased from about $69 billion a year to more than $1.8 trillion." See creditcards.com for broad statistics on credit cards. (back)

11. With inflation kept in check due to downward pressures on wages and the growing import of ever-cheaper consumer products, the Fed has been able to keep the federal funds rate low, slashing it even more in times of recession (e.g., 1975, 1982, 1989, 2001, 2007) -- see Fed Rates and the actions taken by the Federal Open Market Committee.

Fiscal policies include the full deduction of interests paid on mortgages, and an entire panoply of tax credits that are offered to home buyers in various circumstances (first-time buyers, etc.). (back)

12. See "Bill Clinton's drive to increase homeownership went way too far," by Peter Coy, Business Week, February 27, 2008, and the remarks on homeownership by George W. Bush at the Department of Housing and Urban Development, June 18, 2002 (i.e., in the midst of a recession). (back)

13. For a very detailed analysis of the crisis in the U.S., I highly recommend the work of Onubre Einz published at criseusa.blog.lemonde.fr on the Web site of Le Monde. Regarding real estate policies, consumerism, private and public debts, and wages, please refer to "Faut-il dégrader la dette souveraine des USA ou des Trois Krash financiers?", March 21, 2010. Einz's research and analysis are quite comprehensive and comprehensible, even for people who have no economic background. His work would certainly deserve to be translated in English. (back)

14. This graph, developed by the author, is only an approximate representation of five trends that have taken place in the USA in the last 40 years. It is statistically researched but not statistically formulated -- and the author does not profess to be a graphic designer! It is an aperçu of an historical period. (back)

15. Note that public debt began to explode under the Reagan administration and has grown even further after the public bailout of private financial interests (TARP). Note too that the debt grew commensurably with the tax cuts showered upon the wealthy, those people who needed those "breaks" the least. (back)